The ongoing disruption across the Middle East is now sending shockwaves far beyond the region itself, with upstream impacts emerging across air cargo networks, ocean shipping services and global freight pricing.

What began as a regional security crisis affecting Gulf airspace and the Strait of Hormuz is increasingly triggering structural changes in how global supply chains move cargo between Asia, Europe and the Americas.

Carriers and airlines are rapidly restructuring networks, while a growing number of emergency surcharges are being introduced as transport providers attempt to offset rising operational risks and fuel costs.

Air cargo networks feel the strain

Air cargo capacity has begun to stabilise slightly, but significant gaps remain in global lift availability.

Global air cargo capacity is currently down around 8%, improving from the 18% decline recorded earlier in the week. However, the regional disruption remains severe.

Outbound capacity from the Middle East to Europe remains 52% below normal levels, although this is an improvement on the 61% reduction seen earlier in the crisis.

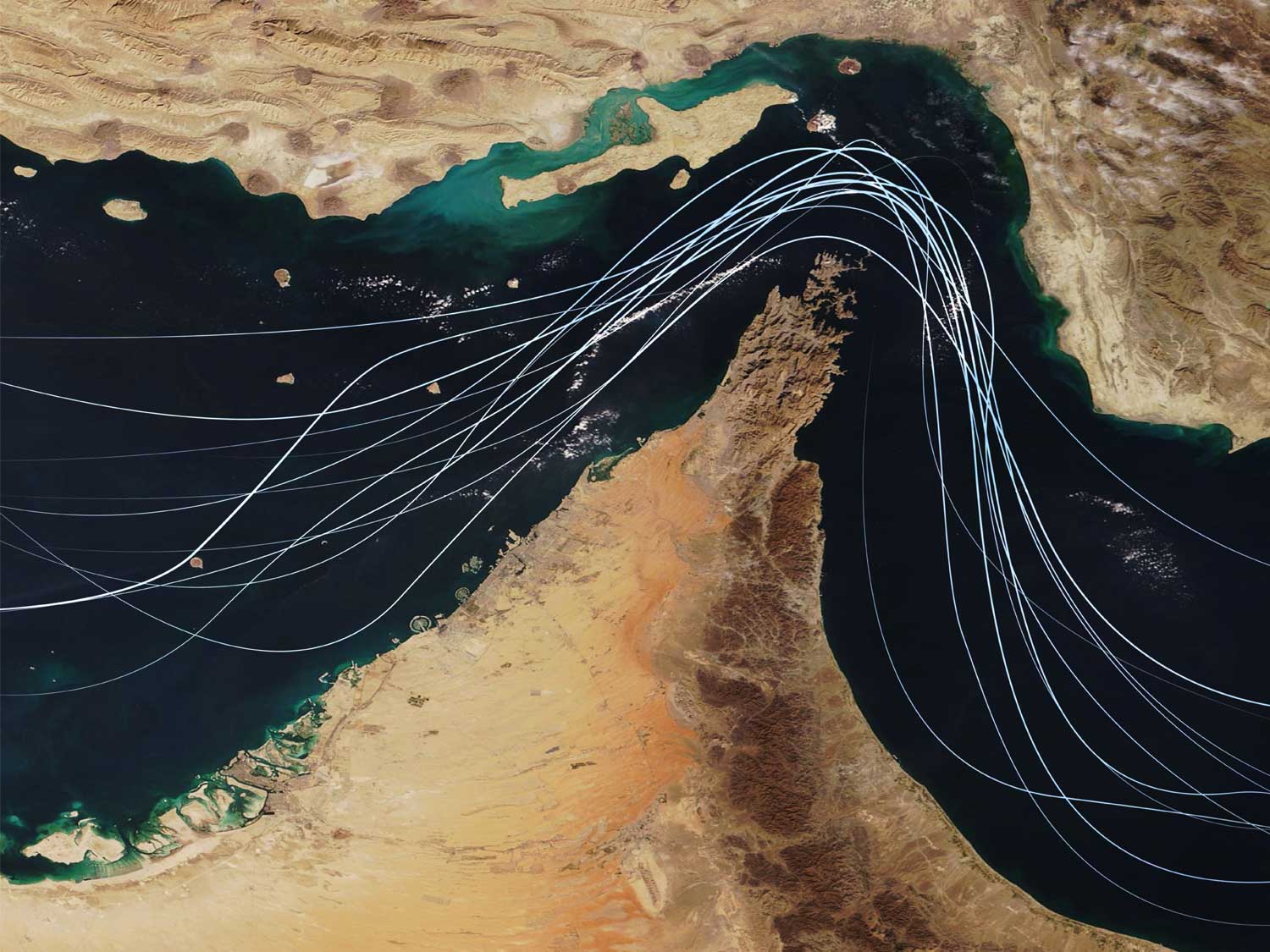

At the same time, capacity from Asia Pacific to the Middle East remains 57% lower week-on-week, reflecting the continued disruption to key Gulf hub airports.

To compensate, airlines have increased direct Asia–Europe flights by around 14%, bypassing traditional stopovers in Dubai, Doha and Abu Dhabi and operating longer non-stop sectors.

However, direct flying cannot fully replace the connectivity normally provided by the Middle East’s hub-and-spoke air cargo networks.

Approximately a quarter of China–Europe air cargo capacity normally transits the Middle East, meaning the sudden loss of these hubs is creating structural gaps in the global network.

South Asia exports under particular pressure

The disruption is particularly acute for exporters across South and Southeast Asia, where cargo flows to Europe and North America rely heavily on Middle Eastern transit hubs.

Across South Asia–Europe corridors, available cargo tonne kilometres (ACTK) have fallen by 39%, leaving shippers scrambling to secure alternative routings.

Air cargo markets across the Indian Subcontinent and Bangladesh are already feeling the secondary effects.

Export capacity from Dhaka has tightened significantly, pushing airfreight rates up by roughly 20%.

In India, where many cargo services traditionally route via Gulf hubs, capacity constraints are becoming increasingly visible. Several major origins are now overbooked, some locations have temporarily stopped accepting cargo for five to seven days, and freight rates have increased by two to three times on certain lanes.

As capacity normally routed through the Middle East disappears, cargo destined for Europe and North America is expected to begin stacking up at Asian airports, creating a growing imbalance between available lift and cargo demand.

Early signs of pricing pressure are already emerging.

Spot rate indices have increased 2% from China to North America, 7% to Northern Europe, and 3% eastbound across the Atlantic.

The developing supply-demand imbalance is drawing comparisons with airfreight market conditions seen during the COVID-19 pandemic, when ocean disruptions pushed large volumes of cargo into the air freight market and triggered rapid rate increases.

Disruption spreads through global shipping networks

The ocean freight sector is experiencing a similar cascade effect.

Maritime tensions intensified further this week when the 1,700-TEU container vessel Safeen Prestige was struck by a missile in the Strait of Hormuz, bringing the total number of vessels hit during the crisis to six tankers and one container ship.

Although only a small proportion of the global fleet is physically located in the immediate risk zone, the operational consequences extend much further.

Currently around 2% of the global container fleet is located inside or near the Persian Gulf.

However, the wider network impact extends far beyond those vessels.

A total of 124 liner services include at least one Arabian Gulf port in their scheduled rotations, representing:

- 520 container vessels

- 3.6 million TEU of deployed capacity

As a result, the current disruption is directly affecting more than 10% of the global container shipping fleet by deployed capacity.

Carriers are already restructuring services, redeploying vessels and adjusting port rotations across multiple trade lanes as they attempt to maintain network stability.

Emergency surcharges begin to emerge

Alongside operational disruption, shipping lines have begun implementing a growing range of emergency surcharges linked to security risks, fuel costs and network congestion.

These charges are appearing under several different names, including:

- ECS – Emergency Conflict Surcharge

- WRS – War Risk Surcharge

- EFS – Emergency Fuel Surcharge

- EFQ – Emergency Fuel Quarterly surcharge

While terminology varies, the purpose is broadly similar: to offset the additional costs associated with longer sailing distances, higher insurance premiums and volatile fuel markets.

In some cases, the surcharges being discussed across the market are significant and may reach four-figure levels per container, depending on the trade lane, equipment type and carrier policy.

Because these charges differ between carriers and routes, shippers may encounter multiple surcharges applied simultaneously as conditions evolve.

Alongside new surcharges, carriers are also introducing operational measures designed to manage equipment supply and limit container accumulation at intermediate ports.

In one recent example, a major carrier has introduced a requirement for import containers discharged at certain ports to be collected from the quay within 48 hours.

Failure to remove containers within that timeframe may trigger additional charges, which in some cases are in a substantial four figure range.

Cargo backing up upstream

The ripple effects are already visible at origin.

In Bangladesh, more than 1,000 containers are currently stranded at Chittagong port and inland depots, while hundreds of containers already shipped remain stuck at Middle Eastern ports or on vessels awaiting discharge.

Similar pressures are beginning to appear at other Asian export hubs as Gulf-bound cargo stalls and vessels adjust schedules.

Nearly every major Asia export port is now experiencing some level of disruption, either through delayed sailings, suspended services or uncertainty around onward routing.

As shipping lines and airlines continue restructuring their networks, the full impact is expected to spread further across global supply chains.

Ocean carriers may redeploy vessels across Asia–Europe and Asia–US trade lanes, while airlines continue adjusting long-haul flight paths to compensate for the loss of Gulf connectivity.

Managing disruption

In light of the rapidly evolving situation, Metro is working closely with customers to assess the need for contingency airfreight on a shipment-by-shipment basis.

Our team can also advise on alternative routing options, particularly for cargo that would normally transit Middle Eastern hubs, helping customers minimise disruption and maintain supply chain resilience.

Customers with shipments moving through the region are encouraged to contact their Metro representative to review routing options and obtain the latest operational guidance.