The latest ceasefire agreement between Israel and Hezbollah, alongside the broader US/Iran framework aimed at ending months of regional conflict, has improved sentiment across energy and freight markets.

Oil prices have retreated, financial markets have stabilised and hopes are growing that the Strait of Hormuz could gradually reopen to normal commercial traffic. Yet for supply chains, the crisis is entering a recovery phase rather than reaching a conclusion.

While diplomats work to turn temporary agreements into lasting settlements, the operational reality remains far more complicated. Shipping lines, insurers and logistics providers are preparing for a lengthy and uneven normalisation process rather than a swift return to pre-crisis conditions.

Diplomacy has moved faster than logistics

The new ceasefire between Israel and Hezbollah removes one of the biggest threats to wider regional stability and supports the broader US-Iran agreement. However, restoring confidence across global transport networks will take far longer than negotiating peace terms.

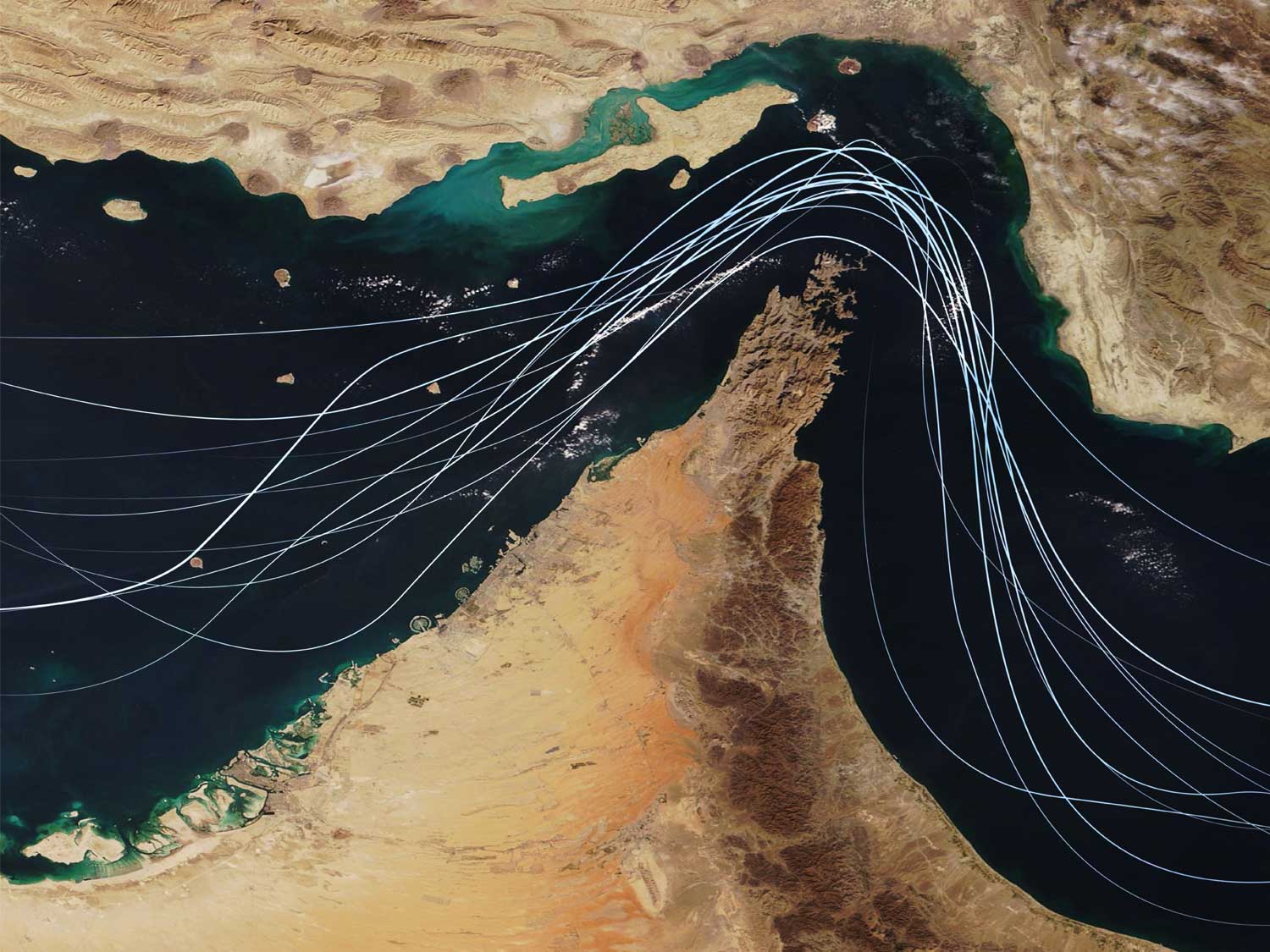

Although limited vessel movements have resumed, hundreds of ships remain affected by months of disruption and maritime authorities continue to treat the Strait of Hormuz with caution. Mine clearance operations, traffic management measures and elevated insurance requirements mean normal trading conditions remain some way off. Even where vessels are moving, transit remains slower and more tightly controlled than before the conflict.

Gulf supply chains face months of adjustment

Importers and exporters serving the GCC area, including major markets such as Saudi Arabia and the UAE, should not expect an immediate return to normal operations.

Regional carriers, feeder operators and overland transport providers have spent months redesigning networks around restrictions and delays. As cargo begins flowing again, ports and transhipment hubs are likely to experience congestion as stranded containers and equipment gradually work their way through the system.

Schedule reliability will improve, but only progressively. Backlogs accumulated over several months cannot be unwound in a matter of weeks, and businesses serving Gulf markets should continue planning for volatility through the summer.

Energy costs remain a major risk

Even though oil prices have fallen on hopes that hostilities are easing, energy markets remain highly sensitive.

Around one-fifth of global oil supply normally moves through the Strait of Hormuz. Any delays to reopening, security incidents or setbacks in ceasefire negotiations could quickly reverse recent gains.

Bunker fuel prices remain well above pre-crisis levels, while jet fuel and diesel markets continue to reflect constrained supply and cautious inventories. Fuel costs remain one of the largest components of transport pricing, meaning surcharges and cost pressures are unlikely to disappear quickly.

Airlines are closely monitoring fuel costs as they finalise winter schedules. Higher operating costs could place further pressure on passenger capacity, with consequences for belly-hold airfreight space.

Road freight operators face similar concerns. Diesel prices remain vulnerable to energy market swings, while ongoing uncertainty continues to influence transport costs across Europe and Asia.

Meanwhile, supply chains that have adapted to months of disruption are unlikely to reverse course overnight. Alternative routings, additional inventories and diversified sourcing strategies developed during the crisis are likely to remain part of many companies' long-term risk management plans.

Stability may return, but gradually

The ceasefires between Israel and Hezbollah and the wider US-Iran framework represent meaningful progress, despite the postponement of direct talks between the US and Iran.

However, diplomacy has moved faster than physical supply chains.

Shipping schedules, equipment availability, insurance markets and energy supplies all require time to normalise. The coming months are likely to bring gradual improvement rather than an immediate reset.

Businesses that continue to secure capacity early, maintain inventory visibility and build flexibility into their transport strategies will be best positioned to complete the transition from crisis management to recovery.

Metro's teams are monitoring developments across ocean, air and road markets in real time. As conditions evolve, we help customers stay ahead of disruption, secure capacity and adapt quickly to changing circumstances.

In volatile markets, resilience comes not from reacting faster than everyone else, but from being prepared before disruption arrives. EMAIL our Managing Director, Andrew Smith to learn more.