Container shipping markets appear to be entering an earlier and increasingly fragmented peak season, as geopolitical disruption, rising fuel costs and tighter carrier capacity management reshape freight demand across major trade lanes.

Bookings on several east-west corridors strengthened earlier than normal during May, with carriers maintaining upward pressure on rates as many importers accelerate shipments ahead of the traditional third-quarter peak season period.

Spot rates on Asia–US west coast services have continued to outperform other major trades, rising around 4% week on week and remaining significantly above levels seen before the escalation of Middle East disruption. Asia–Europe pricing has also strengthened modestly, with rates to North Europe and the Mediterranean increasing as carriers attempt to restore margins through capacity reductions and surcharge increases.

However, broader market conditions remain difficult to interpret. What appears to be an early peak season may ultimately reflect precautionary inventory positioning and front-loading activity rather than sustained end-user demand growth.

Front-loading and disruption are reshaping traditional shipping patterns

A growing number of importers are moving cargo earlier amid concerns that operational disruption, congestion and capacity shortages could intensify later in the year.

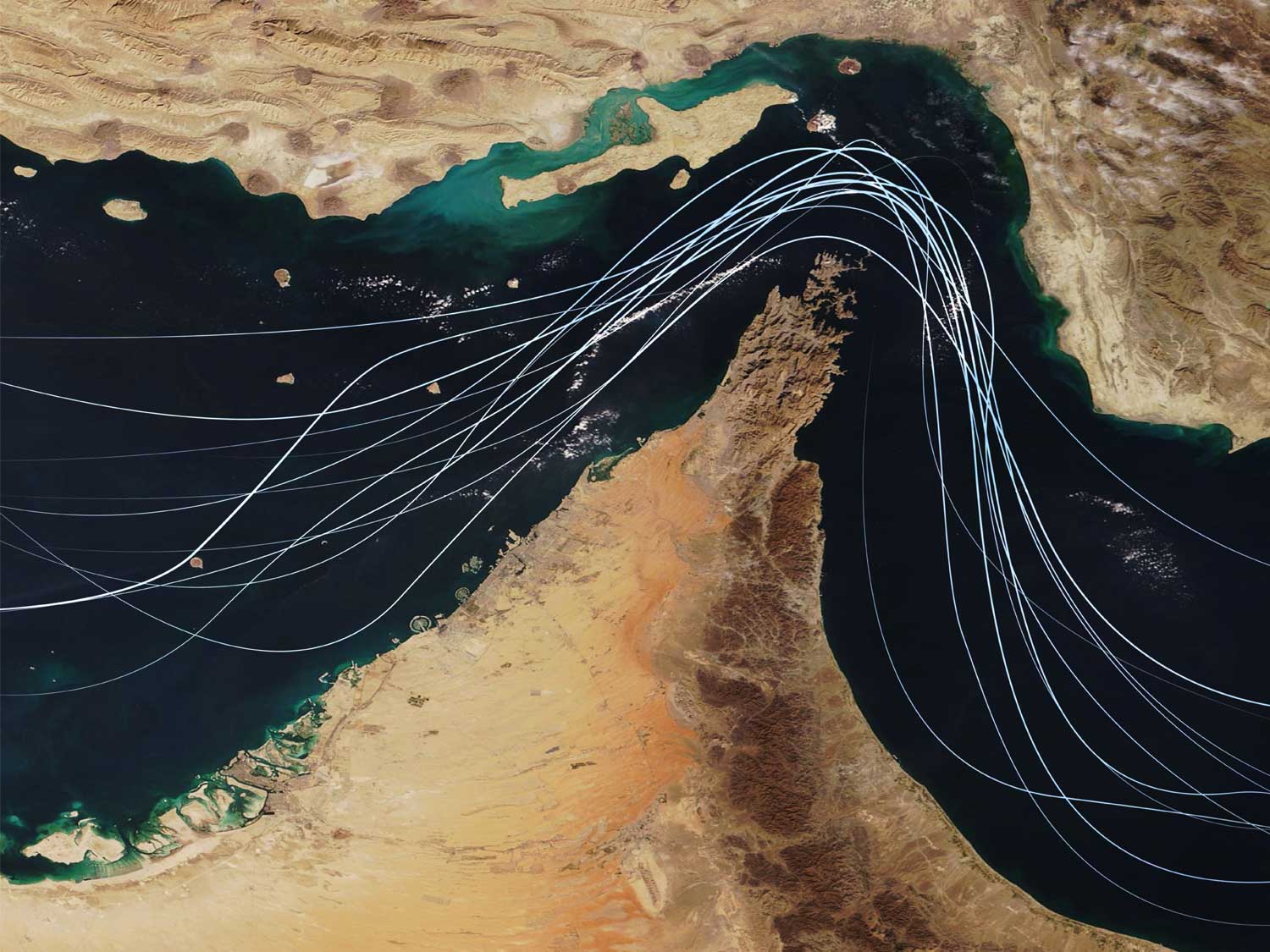

The continuing closure and instability surrounding the Strait of Hormuz is adding further pressure to global freight markets, with around 1.5% of global shipping capacity estimated to be affected directly by disruption linked to the region.

At the same time, higher oil prices are increasing carrier operating costs across both ocean and airfreight markets, while blank sailings are continuing to tighten effective capacity on key trades.

Capacity reductions on Asia–Europe services have become increasingly aggressive in recent weeks, with shipping lines reducing available space to North Europe and the Mediterranean while also introducing additional blank sailings beyond traditional holiday periods.

The result is a more volatile market where shipment rollovers, reduced allocations and short-notice schedule changes are becoming increasingly common, even where bookings are technically available.

On transpacific trades, carriers have also maintained relatively firm control over available capacity following post-Lunar New Year service adjustments, helping sustain pricing despite ongoing uncertainty around underlying consumer demand.

Additional surcharges introduced on Asia–US services suggest carriers expect demand to remain comparatively elevated through the summer period.

Many importers remain cautious about underlying demand, particularly in Europe where economic conditions remain comparatively weak and pressure on household spending continues to affect purchasing behaviour.

This creates the possibility that some businesses could be holding elevated inventory levels later in the year, potentially resulting in a delayed, compressed or weaker traditional peak season across certain sectors.

Metro survey highlights cautious but stable demand expectations

Early findings from Metro’s ongoing customer survey reflect this more balanced outlook.

Around 38% of respondents currently expect freight volumes to remain broadly stable over the next 12 months, while a similar percentage expect volumes to increase slightly. Less than 1/8 anticipate a significant decrease, while none expect a significant increase in activity.

The findings suggest that many businesses are not currently anticipating a dramatic peak season surge, but instead expect relatively stable trading conditions alongside continued disruption and cost pressure.

At the same time, respondents indicate that ongoing instability across global supply chains is continuing to influence inventory planning, shipping schedules and freight costs.

The divergence between Asia–US west coast and Asia–Europe markets highlights how uneven global freight conditions have become. Rather than moving in a single direction, pricing and demand are increasingly being shaped by regional economic performance, inventory strategies and trade lane-specific operational risks.

Sea–air solutions gaining attention as airfreight costs surge

The disruption is also influencing modal shift decisions.

With the average airfreight rate out of Asia-Pacific over 40% higher than last year shippers are increasingly exploring sea–air solutions to balance cost, speed and reliability.

Airfreight rates have risen sharply as fuel surcharges, restricted airspace and tighter capacity continue to affect global networks. At the same time, ongoing Red Sea diversions are keeping some ocean transit times above 50 days on Asia–Europe services.

For many retail, fashion, e-commerce and consumer goods shippers, sea–air services are becoming an increasingly valuable tactical solution where traditional airfreight costs are difficult to absorb but ocean transit times remain commercially challenging.

For shippers, the key challenge may now be timing. If front-loading activity continues through the early summer period, demand on some corridors could remain firmer for longer than normally expected. However, weaker consumer demand and elevated inventory levels could also limit the scale of any traditional late summer or autumn rebound.

Metro’s survey remains open, and businesses are encouraged to share their expectations and experiences, together with insights into current market conditions, operational pressures and changing supply chain requirements. The survey also provides an opportunity for customers to share feedback on Metro’s performance and highlight where additional support or solutions could help strengthen supply chain operations.

Through proactive capacity planning, multimodal air, sea and sea-air routing options and contingency-focused supply chain support, Metro helps customers respond more effectively to disruption, changing demand patterns and ongoing peak season uncertainty. EMAIL Managing Director, Andrew Smith, to learn more.